Abstract

In Kenya, digital financial services have transformed how small and medium-sized businesses (SMEs) access capital, manage their day-to-day operations, and expand their businesses. Services like M-Pesa, mobile banking, and fintech apps have enabled more people, particularly young individuals and women, to access financial tools. These services have made it easier for entrepreneurs to start and grow their businesses. However, there are still challenges, such as not knowing much about digital tools, rules about how financial services are managed, and data protection and regulation. This article looks at Kenya’s fintech environment, talks about how it’s helping SMEs, and gives ideas for people in charge of policies and business owners. It also encourages new ideas that are fair, fit well with local communities, and can be shared across Africa to enhance sustainable development.

Kenya is known around the world for being an early leader in mobile money. M-Pesa, which started in 2007, helped start the growth of fintech in Kenya. It allowed users to send, receive, and save money using their mobile phones, which made it easier for people, especially those living in rural areas, to access basic financial services. Over the years, this has grown into a lively fintech scene. (FinAccess Survey)

Kenya now has more than 200 fintech startups, many of which are focused on helping small businesses, giving out digital loans, and making payments easier. (FSD Kenya). The Central Bank of Kenya (CBK) has helped this growth by creating the Regulatory Sandbox Framework and the Digital Credit Providers (DCPs) Regulations (2022) to make sure these new services are fair and responsible in the business of lending money. Kenya’s success with fintech stems from several things: most people have mobile phones, a huge innovative private sector, and people want better, more flexible, and inclusive ways to manage their finances. (Central Bank of Kenya). Platforms like Mshwari reflect this success by enabling users to save as little as Ksh. 10 while still earning interest, hence encouraging a saving culture among informal traders, boda boda riders, and students. (FSD Kenya 2022)

Small and medium enterprises (SMEs) are very important to Kenya’s economy. They account for over 90% of all businesses and bring in about 30% of the country’s total GDP. (World Bank). However, access to credit from traditional banks is still out of reach for many, particularly small businesses and informal entrepreneurs. Banks often require a lot of proof that you can pay back a loan, and they have complicated rules that make it hard for many business owners to get loans. Similarly, a cyber café owner in Kisumu shared how he used Fuliza to maintain internet bundles during slow months, allowing him to stay operational, but he noted how the accumulated debt became overwhelming without clear repayment terms. (Business Daily Africa, 2023)

Mobile-based financial services have helped fill this gap, but not without creating fresh challenges and risks. Certain fintech companies impose high interest rates, provide unclear cost structures, and employ harsh debt recovery practices. Furthermore, many people in rural areas or those who are new to technology often lack the skills to navigate these tools securely and express concerns about cybersecurity threats and fraud. (FSD Kenya)

An entrepreneur from Nakuru who runs a small dairy business said:

“Getting a bank loan was impossible, but through a digital app, I got a small loan to buy a milk cooler. That’s how I grew my business. But repaying it was stressful; the fees were confusing. ”

This shows that while it’s important to make loans more available, it’s also important to make sure people are protected when using them.

Take the story of Mama Zawadi, a business owner in Nairobi who makes natural skincare products using ingredients from her community. When the pandemic hit and her in-person sales dropped, she used Lipa Na M-Pesa to accept payments, partnered with Pesapal for online transactions, and got a loan from Tala to keep her business running. In six months, she started selling online, and her revenue went up by 40%. Fintech not only kept her business going but also helped her grow it to a national level. This is just one of many similar stories in Kenya. Here, technology is not just a tool; it’s a key part of how businesses succeed.

These solutions reflect local innovation that fits the real needs of Kenyan businesses.

They combine modern tools with traditional ways of thinking and doing business, leading to growth that works well with local culture and the economy.

To make fintech even more helpful for Kenya’s small and medium businesses, several steps could be taken:

It’s important to teach more people, especially those in rural areas, how to use digital tools.

This can be done through teamwork between fintech companies, schools, and government agencies. This way, entrepreneurs will know how to use fintech safely and get the most out of it. (FinAccess Kenya). One such initiative is Equity Bank’s “Fanikisha Jamii” program, which partners with local trainers to teach digital banking to women selling groceries and textiles in Gikomba market. (Equity Group 2025)

While the licensing of digital credit providers is an important regulatory step, it must be complemented by comprehensive frameworks that aim to curb exploitative lending practices and ensure robust consumer protection. In addition, strict adherence to the provisions of the Data Protection Act from 2019 is essential to safeguard the privacy and security of users’ data within the digital finance ecosystem. (Central Bank of Kenya)

Fintech must continue creating products that are useful for Kenyan people, such as loans that align with agricultural seasons or savings groups that function like traditional community savings chamas. Using knowledge from local practices and social finance can help create better solutions.

Women often find it harder to get financial support. There are products like those from Grace Health, which link credit to health services, or savings tools that offer support for motherhood. These kinds of products can help women succeed in business and also make a bigger impact. (Women Tech Network). Additionally, digital Sacco platforms like Chapchap support women in rural areas like Bomet and Kitui to pool savings for livestock projects and gain mobile credit history. (Techweez, 2024)

Kenya’s fintech journey isn’t over.

The future includes:

Kenyan fintech companies are also sharing their models with other countries like Uganda and Rwanda. With more investment, assistance from the government-led projects, and responsible innovation, Kenya could help lead the development of financial technology across the whole continent.

Conclusion

Digital financial services are changing the way small and medium businesses operate in Kenya.

Even with the difficulties, the way fintech and local communities work together gives a strong example of how to help everyone grow together. As fintech grows, it’s important to make sure it works well with local culture, is fair, and is available to everyone. This way, the benefits of fintech can reach every part of the country, and maybe even the whole continent.

Visual Breakdown of Fintech Services in Kenya

Source: Compiled estimates based on FSD Kenya, CBK, and industry reports.

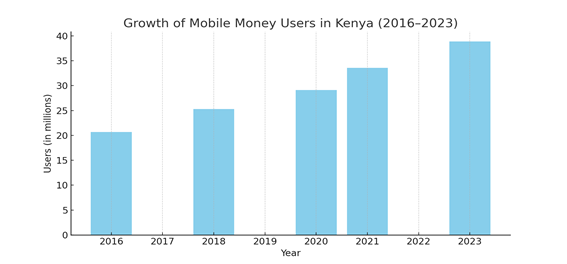

Mobile money user growth in Kenya (2016-2023)

Source: FinAccess & Central Bank of Kenya (2016–2023)

References

“How Can Fintech Tools Break Barriers to Women’s Economic Empowerment?” Women Tech Network,

https://www.womentech.net/en-za/how-to/how-can-fintech-tools-break-barriers-womens-economic-empowerment. Accessed July 16th, 2025.

“How Equity Bank Is Enabling Women Entrepreneurs to Succeed in the Kenyan Market.” HapaKenya, 17 Nov. 2022,

https://hapakenya.com/2022/11/17/how-equity-bank-is-enabling-women-entrepreneurs-to-succeed-in-the-kenyan-market/. Accessed July 16th, 2025.

“Microfinance Institutions Drive Women’s Economic Growth in Kenya.” Kenya Forum,

https://www.kenyaforum.net/economy/microfinance-institutions-drive-womens-economic-growth-in-kenya. Accessed July 18th, 2025.

Business Daily Africa, Techweez, and The Standard. Various articles, 2023–2024.

Central Bank of Kenya. Annual Report. 2023.

FinAccess Survey. 2021, 2023.

FSD Kenya. Digital Finance and Inclusion Reports. 2022.

Grace Health. Grace Health, https://www.grace.health. Accessed July 16th, 2025.

GSMA. Mobile Money Metrics. 2023.

World Bank. Africa Pulse Report. 2023.

FSD Kenya. Digital Finance and Inclusion Reports. 2022.

How Fuliza Is Changing Informal Lending Habits.” Various articles, 2023

Fanikisha Jamii Program Overview. 2025. https://equitygroupholdings.com/ke/borrow/chamagroup/

Author Bio

Ng’ang’a Serah Wacu is a certified professional mediator and law graduate with a keen interest in digital innovation, social justice, and economic inclusion. She holds a certificate in Data Privacy and has led impactful projects under the Millennium Fellowship Network, advancing gender equality and poverty reduction across local communities. Serah is driven by the belief that technology and law can work together to unlock opportunity, especially for underserved groups. Through her work, she brings a blend of legal expertise, advocacy, and storytelling to spotlight homegrown solutions and amplify voices that are often overlooked in Africa’s development conversations.

How do you find this report?

Leave a reply

Rate the author

Africa should focus on value-added processing instead of exporting crude vegetable oil. By refining and…

Assignment Title: Raising awareness on our member education and development activities Assignment Duration: 8 weeks…

Tasks Performed Promoted two blog discussion topics on the AAE website: Turning Ideas into Impact:…

Addis Ababa, Ethiopia & Dubai, UAE – Sep 17, 2025 Meltex Textile Apparel Manufacturing and…

Volunteer Group: AAE Volunteers Assignment Period: June–September 2025 Report Type: Final Report Introduction: As an…

💬 Discussion Prompt Hello everyone, As part of my awareness-raising mission with AAE, I’d like…

{kind=link}